Why Budgets Fail (And What Actually Works)

Most budgets fail within weeks. Not because the math was wrong, but because they were designed to fight human psychology instead of work with it.

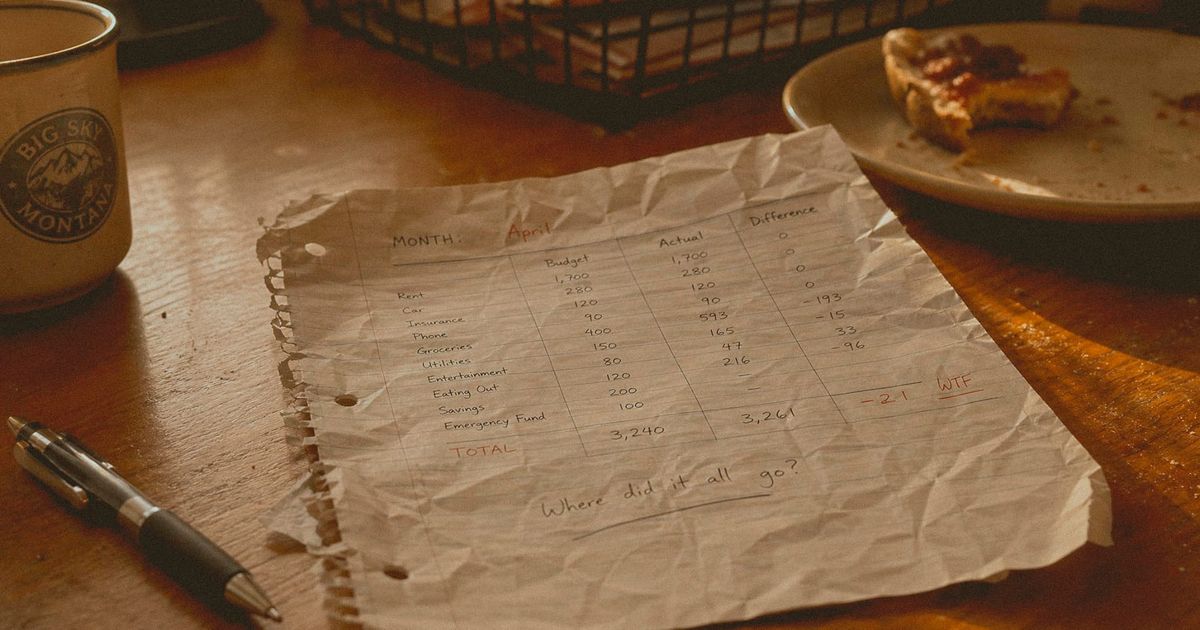

Most people who try to budget fail within the first few weeks. Not because they lack discipline, and not because the numbers didn't add up. The math is usually fine.

Budgets fail because they are almost universally designed to work against how the brain actually handles money, restrictions, and willpower. Understanding why budgets fail changes what you build instead, and what actually works looks quite different from the standard approach.

The diet problem

The most useful analogy for why traditional budgets fail is dieting. Restrictive diets work in the short term and fail in the long term at roughly the same rate as restrictive budgets, and for the same reasons.

When something is forbidden, the brain registers it as a loss. Loss aversion, the tendency to feel losses more intensely than equivalent gains, makes restrictions feel more painful than the actual sacrifice warrants. The person on a strict diet doesn't just want the food less. They want it more, because restriction has made it feel more valuable.

The same mechanism operates with money. A budget that categorizes most enjoyable spending as off-limits doesn't produce discipline. It produces deprivation, followed by rebellion, followed by abandonment of the plan entirely.

Researchers call this the all-or-nothing effect: a single violation of a strict rule tends to trigger full collapse rather than minor correction. One dinner out doesn't slightly derail a budget. It becomes the reason the whole system gets abandoned. The logic is: I already broke it, so what's the point?

The willpower problem

Traditional budgeting requires constant active decision-making. Every purchase needs to be evaluated against the budget, tracked, and consciously approved. That approach runs directly into one of the most replicated findings in behavioral economics: ego depletion.

The idea, supported by research from Roy Baumeister and colleagues, is that self-control draws on a limited cognitive resource. Every act of willpower, every decision that requires conscious restraint, uses some of that resource. As it depletes through the day, the ability to make disciplined financial decisions deteriorates.

This is why financial willpower tends to collapse at night, after a long or difficult day, or in emotionally taxing periods. The resource that would normally override the impulse to spend is already depleted by everything else that required discipline. The budget was perfectly reasonable at 9am. By 9pm it doesn't stand a chance.

A system that requires constant willpower will fail whenever willpower runs short, which is regularly.

The tracking problem

Tracking every purchase feels manageable in theory. In practice, it creates a relationship with money that most people find psychologically exhausting.

Research on what's called budget fatigue suggests that the cognitive load of detailed tracking, combined with the negative emotions that arise from confronting every spending decision, causes most people to disengage rather than persist. The tracking becomes a source of shame and stress rather than useful information.

There's also a timing problem. Traditional tracking is retrospective. You record what happened after it happened. By the time you know you've overspent in a category, the spending has already occurred. The information is accurate but arrives too late to change the behavior it's documenting.

What actually works

The approaches that tend to produce durable results share a common feature: they reduce the number of decisions that require willpower, rather than relying on willpower to be consistently present.

Automation first. The most reliable financial behavior is behavior that happens without a decision. Automatic transfers to savings on payday, before the money enters a spendable account, work because they remove the choice entirely. The money is gone before the brain registers it as available. Research consistently shows that automatic savings produces higher savings rates than equivalent willpower-based approaches.

Spend freely within a defined envelope. Instead of tracking every category, identify one or two areas where overspending has historically been the problem and set a fixed envelope for those. Everything else is untracked. This concentrates the willpower where it matters and removes the cognitive load from everywhere else.

Design for failure recovery, not failure prevention. A budget that collapses when violated once is badly designed. The more useful design question is: when I go over in a category, what happens next? Building in a recovery mechanism, rather than a system that only works when perfectly followed, produces much more durable financial behavior.

Match the system to how you actually think. Someone who thinks in percentages does better with percentage-based budgeting. Someone who thinks concretely does better with fixed dollar amounts per category. The most sophisticated system that you don't use is worse than the simplest system that you actually follow.

The reframe worth trying

The goal of a budget isn't to restrict what you spend. It's to ensure that your spending reflects what you actually want your money to do.

That reframe matters practically. Restriction-framed budgets trigger loss aversion and rebellion. Direction-framed budgets, where the question is where do I want this money to go rather than what am I not allowed to spend, produce less psychological resistance and more consistent follow-through.

A budget that works isn't necessarily more detailed or more disciplined than one that doesn't. It's better designed for the brain that has to follow it.

Questions about budgeting and why it fails

Why do budgets fail?

Budgets typically fail because they're designed to fight human psychology rather than work with it. The most common failure mechanisms are the restriction-rebellion cycle driven by loss aversion, ego depletion from constant willpower-based decision-making, and budget fatigue from detailed tracking that creates shame rather than useful information. A budget that requires consistent active discipline will fail whenever discipline is in short supply, which is regularly.

What is the all-or-nothing effect in budgeting?

The all-or-nothing effect is the tendency to abandon a budget entirely after a single violation, rather than treating it as a minor deviation to correct. It's driven by the same psychological mechanism as diet abandonment after one cheat meal: the brain treats the violation as proof that the system has failed, which makes continuing feel pointless. Building recovery mechanisms into a budget, rather than designing it to only work when perfectly followed, addresses this directly.

What is ego depletion and how does it affect budgeting?

Ego depletion is the finding from behavioral economics that self-control draws on a limited cognitive resource that depletes with use. Every act of willpower, every decision requiring restraint, uses some of that resource. Budgets that require constant active decision-making perform well when that resource is full and fail when it's depleted, which tends to happen later in the day, after difficult periods, and during emotionally taxing times. Systems that automate financial behavior rather than relying on willpower work better precisely because they don't depend on this resource being available.

What budgeting method actually works?

The approaches with the most durable results tend to reduce required decisions rather than require consistent willpower. Automatic savings transfers before money enters spendable accounts, spending envelopes that concentrate attention on one or two problem categories rather than tracking everything, and systems designed to recover from violations rather than collapse under them, tend to outperform detailed traditional budgets. The most important variable is whether the system matches how you actually think, not how sophisticated it is.

Is budgeting necessary for financial health?

Not in the traditional sense. The goal of financial health, spending in ways that align with your values and building toward future security, can be achieved through various systems. Automation, simplified envelopes, percentage-based approaches, and regular spending reviews all serve the same function as detailed budgets without requiring the same cognitive load. What matters is having a system, not which specific system it is.